GST/HST Registration for Self-Employed Canadians: When the $30,000 Rule Applies

Self-employed in Canada? Learn when GST/HST registration is required, how the $30,000 small supplier threshold works, and what to do if you registered late.

By Majdi Ibrahim, CPA | Majdi Ibrahim, CPA Professional Corporation | Ottawa, Ontario

GST/HST registration is one of those small-business tax issues that seems simple until the timing matters.

Most self-employed Canadians have heard some version of the “$30,000 rule.” The problem is that the rule is often repeated in a way that leaves out the details that actually matter: what counts toward the threshold, whether the amount is based on profit or revenue, what happens if you cross the threshold in one busy quarter, and whether you should register voluntarily before CRA requires it.

If you are a freelancer, consultant, contractor, online seller, designer, coach, tradesperson, or other self-employed person in Ottawa or elsewhere in Canada, this article walks through the practical GST/HST registration rules and the common traps to avoid.

For a broader filing-season overview, see our self-employed tax checklist. This article focuses specifically on GST/HST registration for most self-employed businesses. It does not cover every special rule for charities, public institutions, listed financial institutions, non-residents, platform operators, or detailed place-of-supply questions.

At a Glance

The usual GST/HST small supplier threshold is $30,000. For most businesses, you generally do not have to register while your taxable supplies are $30,000 or less over four consecutive calendar quarters. The threshold is based on revenue from taxable supplies, not profit. Expenses do not reduce the threshold calculation. Crossing $30,000 in one calendar quarter is different. If you exceed the threshold in a single quarter, you may have to register and start charging GST/HST on the sale that pushed you over. Taxable does not mean “taxable income.” For GST/HST purposes, taxable supplies include zero-rated supplies. Exempt supplies are treated differently. Voluntary registration can be useful, but it adds responsibility. It may allow input tax credits, but it also means filing returns, charging GST/HST where required, and remitting on time.

The Basic Rule: Do You Make Taxable Supplies?

Before looking at the $30,000 threshold, start with a simpler question: are you making taxable supplies in Canada?

For many self-employed people, the answer is yes. Consulting services, design work, marketing services, coaching, many trades services, and many online sales are generally taxable supplies for GST/HST purposes.

But not everything is taxable. Some supplies are exempt. CRA gives examples such as many health, medical, and dental services performed by licensed practitioners for medical reasons, and long-term residential rentals. If your business provides only exempt supplies, CRA generally says you cannot register for a GST/HST account.

That distinction matters. A self-employed consultant in Kanata selling taxable services is not in the same GST/HST position as a landlord earning long-term residential rent. If rental income is part of your situation, our article on rental income and taxes in Canada may be a better starting point.

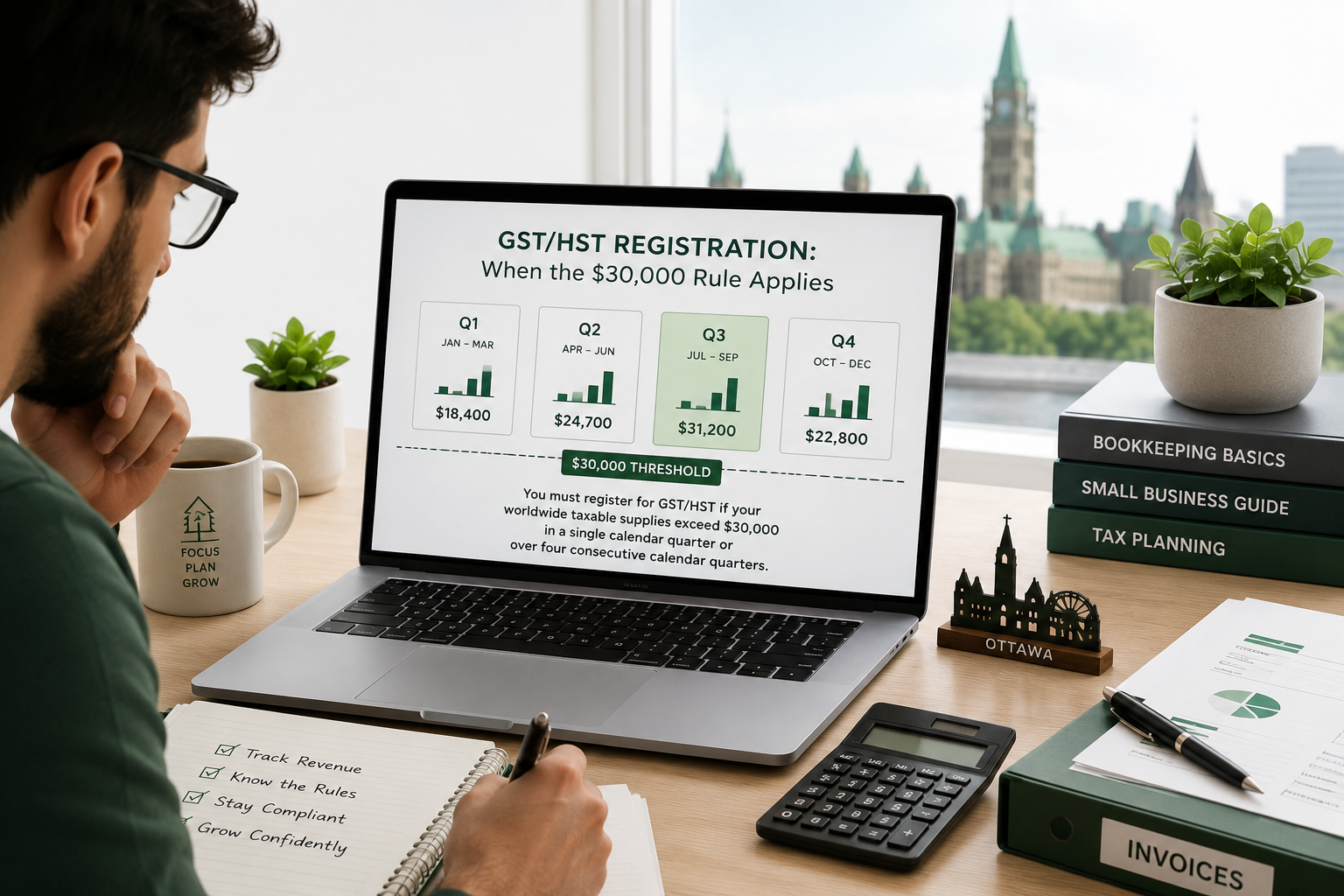

The $30,000 Small Supplier Threshold

For most businesses, you are generally considered a small supplier if you do not exceed $30,000 in taxable supplies over four consecutive calendar quarters.

Two parts of that sentence matter.

First, it is taxable supplies, not net income. If you invoice $35,000 and spend $20,000 on business expenses, you have not reduced your GST/HST threshold calculation to $15,000. The threshold looks at revenue from taxable supplies before expenses.

Second, it is based on calendar quarters, not your personal tax year or the date you started tracking it.

Calendar quarters are:

- January 1 to March 31

- April 1 to June 30

- July 1 to September 30

- October 1 to December 31

This is why GST/HST can sneak up on people. A self-employed person may think, “I did not earn $30,000 last year,” but the actual test may look at four consecutive calendar quarters that cross over two calendar years.

What Counts Toward the Threshold?

CRA says sole proprietors include revenue from worldwide taxable supplies from all their businesses and associates, where applicable, for purposes of the small supplier threshold. That is a threshold calculation point; it does not mean every sale outside Canada is automatically charged Canadian GST/HST.

In practical terms, this means:

- use revenue before expenses

- include taxable supplies from all your self-employed activities

- include zero-rated supplies

- do not include exempt supplies

- do not include sales of capital property, financial services, or goodwill from the sale of a business

This is one reason clean bookkeeping matters. If your records do not separate taxable, exempt, and zero-rated sales clearly, it becomes harder to know when you actually crossed the line. For more on recordkeeping and monthly support, see our guide to bookkeeping costs for small businesses.

The Timing Trap: One Quarter vs. Four Quarters

The GST/HST registration timing rules are where many self-employed people get caught.

If You Exceed $30,000 in One Calendar Quarter

If you exceed the $30,000 threshold in a single calendar quarter, you stop being a small supplier on the supply that made you exceed the threshold.

That means you generally have to start charging GST/HST on the sale that pushes you over $30,000 in that quarter. Your effective date of registration is no later than that date.

Example:

An Ottawa consultant has a very busy quarter:

- January: $8,000

- February: $12,000

- March: $14,000

The March invoice pushes the quarter over $30,000. That invoice may be the one where GST/HST needs to start, not the next invoice.

This is the part many people miss.

If You Exceed $30,000 Over Four Consecutive Calendar Quarters

If you exceed $30,000 over four or fewer consecutive calendar quarters, but not in a single quarter, the timing is different.

In that case, you are generally no longer a small supplier at the end of the month following the quarter in which you exceeded the threshold. Your effective date of registration is no later than the day of the first taxable supply you make after you stop being a small supplier.

Example:

A self-employed designer earns:

- Q1: $7,000

- Q2: $9,000

- Q3: $8,000

- Q4: $9,000

Total over four quarters: $33,000.

The designer did not exceed $30,000 in one quarter, but did exceed it over four consecutive quarters. That creates a registration timing issue after the end of the quarter, not necessarily on the invoice that crossed the four-quarter total.

Voluntary Registration: Should You Register Before You Have To?

If you are still a small supplier, you may be able to register voluntarily if you make taxable supplies in Canada.

Voluntary registration can make sense where:

- your clients are mostly GST/HST registrants who can claim input tax credits

- you have meaningful startup or equipment costs with HST paid

- you want to claim ITCs on eligible business expenses

- you expect to exceed the threshold soon anyway

- you want cleaner systems from the start

But voluntary registration is not automatically better. Once registered, you take on real responsibilities:

- charge GST/HST where required

- file GST/HST returns

- remit amounts collected

- keep proper records

- track input tax credits correctly

If you are below the threshold and your clients are mostly individuals who cannot recover HST, voluntary registration may affect pricing unless your fees are adjusted carefully. That trade-off should be considered before registering.

One more practical point: if you register voluntarily and charge GST/HST, those amounts generally need to be reported and remitted. Charging GST/HST is not something to do informally.

What Happens After You Register?

Once registered, GST/HST becomes part of your normal business system. You collect tax on taxable supplies, track the GST/HST you paid on eligible business expenses, file returns, and remit the net amount.

This is also where deadlines matter. GST/HST filing and payment due dates depend on your reporting period, and missed filing can create penalties and interest. Our article on CRA tax deadlines for small businesses explains the broader deadline problem.

The bookkeeping should make this easy:

- sales should show whether GST/HST was charged

- expense receipts should show GST/HST paid

- exempt or zero-rated supplies should be identified properly

- returns should reconcile to your accounting records

If your records are messy, fix that before the first return becomes a scramble.

What If You Should Have Registered but Did Not?

This is common.

A self-employed person grows gradually, crosses the threshold without realizing it, and continues invoicing without GST/HST. Months later, they discover they should have registered earlier.

The risk is that CRA can assess GST/HST that should have been collected, even if you did not actually charge it to your clients. That can turn into a real cash-flow problem, because the tax may come out of your pocket.

If this has already happened, do not ignore it. The next step is usually to:

- determine the actual threshold-crossing date

- calculate the effective registration date

- review invoices issued after that date

- estimate GST/HST exposure

- review whether input tax credits may reduce the net amount

- decide whether backdating registration or a disclosure approach is needed

If CRA problems are already part of the picture, our guide on how to catch up when you are behind on taxes and our article on the Voluntary Disclosure Program may also be relevant.

Special Situations to Watch

Ride-sharing and taxi services. Taxi operators and commercial ride-sharing drivers have special GST/HST registration rules and may have to register even if they are small suppliers.

Short-term rentals. Airbnb and other short-term rental activity can raise GST/HST issues quickly, especially where revenue grows or the property is not a long-term residential rental. See our article on Airbnb and short-term rental taxes in Canada.

Health services. Many medical and health services are exempt, but not every service provided by a health professional is automatically exempt. Review the specific supply.

Mixed businesses. If you have both taxable and exempt activities, GST/HST gets more complicated. You may need to allocate expenses between commercial and exempt activities for ITC purposes.

Place-of-supply questions. The province, customer location, type of supply, and delivery details can affect which GST/HST rate applies. This article is about registration timing, not a full place-of-supply review.

Ottawa & Area: How This Shows Up in Practice

In Ottawa, this issue often comes up with freelancers, IT consultants, marketing consultants, tradespeople, coaches, creators, and service providers who start small and then have one strong year.

The GST/HST problem is rarely that someone intentionally ignored the rules. More often, the business grew, the owner was focused on clients, and nobody was checking the rolling threshold quarter by quarter.

That is why I like to review GST/HST early with self-employed clients. It is much easier to register at the right time than to reconstruct the threshold six months later with an Ottawa CPA after the invoices have already gone out.

What Happens When You Bring This to Majdi Ibrahim, CPA?

We check whether registration is actually required. We look at your revenue, the type of supplies you make, and whether the $30,000 small supplier threshold has been crossed.

We identify the correct timing. The answer may depend on whether you crossed the threshold in one quarter or over several quarters. We help determine the effective date instead of guessing.

We review voluntary registration. If you are below the threshold, we look at whether voluntary registration makes sense based on your clients, expenses, and growth.

We help clean up missed registration. If you should have registered earlier, we help calculate the threshold date, effective registration date, back-HST exposure, potential ITC support, and the cleanest way to bring the account current.

Book a consultation at www.treehousecpa.com

Frequently Asked Questions

Do self-employed Canadians have to register for GST/HST?

Not always. For most businesses, registration is generally required when you are no longer a small supplier and you make taxable supplies in Canada. Many self-employed people do not have to register while their taxable supplies are $30,000 or less over four consecutive calendar quarters, but there are exceptions and timing rules.

Is the $30,000 GST/HST threshold based on profit or revenue?

It is based on revenue from taxable supplies before expenses, not profit. Expenses do not reduce the threshold calculation.

What happens if I exceed $30,000 in one quarter?

If you exceed the $30,000 threshold in a single calendar quarter, you generally stop being a small supplier on the supply that made you exceed the threshold. You may have to start charging GST/HST on that supply.

Can I register voluntarily for GST/HST before I reach $30,000?

In many cases, yes, if you make taxable supplies in Canada. Voluntary registration may allow you to claim input tax credits on eligible expenses, but it also creates filing, charging, remitting, and recordkeeping responsibilities.

What if I should have registered but did not?

You should review the threshold timing, effective registration date, invoices issued after that date, and potential GST/HST exposure. Depending on the facts, you may need to backdate registration or consider a disclosure approach.

Disclaimer

This article is general information only and is not legal, tax, or accounting advice for your specific situation. GST/HST rules depend on the exact supplies you make, your revenue, timing, and registration status. Speak with a qualified CPA before relying on this information for a decision.